#1 The Gold Rush in the Indian Lending Market

#1 The Gold Rush in the Indian Lending Market

Understanding gold loan fintechs

Index

Gold Market Overview

India’s love story with gold

Gold as an investment product

Gold Loans in India

Market Players

Banks

NBFCs

Fintech Players

Distributor Players

Aggregator Players

Way forward

Competition from substitute products

Maturing Alternate credit assessment models

Need for portfolio diversification

Asset-backed lending platforms

Secured credit cards

Gold Credit Networks

Gold Market

In 1991, India faced its worst financial crisis where the government was pushed to corner due to excess reliance on imports and other external factors like the Gulf War and the collapse of the Soviet Union. The dire situation meant that the Indian foreign exchange reserves could have barely financed three weeks' worth of imports and the government came close to defaulting on its financial obligations.

To tide over the crisis, the Reserve Bank of India had to pledge and airlift 47 tons of gold to the Bank of England and 20 tons of gold to the Union Bank of Switzerland to raise USD 2.2 Billion. The transfer was done in secrecy amidst the 1991 general elections. National sentiments were outraged and there was a public outcry when it was learned that the government had pledged the country's entire gold reserves against the loan. The Chandra Shekhar government which had authorized the airlift collapsed a few months after the incident. This is one of the many interesting chapters in the enduring love story of India and its gold.

As per the World Gold Council, Indian households have the highest reserves of gold (23,000 - 25,000 tonnes) compared to anywhere else in the world. Our annual demand for gold is 700-800 tonnes, and this accounts for 25% of the global demand for gold. WGC expects the demand to reach 950 tonnes per annum by 2021 at an annual growth rate of 35%, with two-thirds of this demand coming from the rural market.

Almost every Indian retail investor either already has gold holdings or is considering purchasing it in the future. To put it simply, Gold is a staple food of the Indian investing diet.

Gold Loans

Almost 70% of the gold loan market in India is unorganized due to a combination of factors:

Predominantly rural demand

Easy access to pawnbrokers/local lenders

Low documentation and effort

Lack of awareness

In the organized market, Indians borrow USD 40 bn a year against their gold. This borrowing is mostly done at specialized NBFCs and Banks. In 2019, the total gold loans outstanding were estimated to be 5.5% of the total gold holdings, indicating a significant market opportunity for new-age lending companies.

The Market Players

Banks

Banks (public, private, small finance, co-op) have a significant advantage over the other lenders in this context as the cost of capital is the lowest for them. However, banks lack the flexibility and quick turnaround time for loan disbursal, features that are very important to this demographic.

Availing a gold loan at a bank branch is not as straightforward as it seems. The branch manager has to ensure the availability of a valuation officer and also the optimal storage facility. They also need to plan for the logistics of transporting the gold to the zonal office post the loan disbursement.

Needless to say, Gold loans present operational headaches and bottlenecks in branch operations for managers (availability of valuation officers, storage facilities, etc.) and hence, managers primarily consider gold loans as a means to fulfill their priority sector lending requirements by offering them for agriculture, MSME, and other such PSL purposes.

Although banks have the financial muscle and (in some cases) the reach to push for organized gold lending, they have shied away from the opportunity due to the specialized nature of the loans and operational headaches associated with this sector.

Specialized NBFCs

Because banks could not support the growing demand for gold loans a few enterprising NBFCs cropped up in the 2000s. In the large puzzle of solving for gold loans they nailed four aspects:

Fast and accurate gold valuation

Faster loan processing (less than 2 hours)

Better customer empathy

Local-level reach

Trustworthy safekeeping facilities

And predictably, despite many challenges like regulatory and market shocks (fluctuations in LTV ratios, suppressed gold prices, restricted credit exposure) the specialized NBFCs have been able to consistently grow at about 35% CAGR over the last 5 years.

The 2 star lenders in this space, have shown impressive growth and have entrenched themselves in the space with aggressive expansion, branding, and promotion activities.

Between FY 19-20 and FY 20-21, Muthoot Finance grew its AUM by 28% to USD 6.9 bn and Mannapuram Finance grew its AUM by 18% to USD 2.5 bn.

The NBFCs liquidity stress (due to the IIFL crash) led to a significant slowdown in fund disbursals as the smaller players were cash-starved. The cost of capital remained relatively stable for large players like Muthoot and Mannapuram but increased for the smaller players.

This has led many of the players to pivot to low ticket size and short-term (3-6 months) tenure loans (higher yields due to capital rotation). NBFCs have also been adopting digital journeys by enabling aadhaar based KYC processes and direct deposits. This has reduced the processing time to less than 2 hours in ‘hub’ branches.

As a smaller player in this category, a new upstart, or a regional/local player; you will struggle with various factors like upfront Capex investment, availability of real estate and trained personnel, higher cost of capital, and (of late) suppressed gold prices leading to higher NPAs. The high upfront cost for geographic expansion and lead time for training personnel also leads to players being restricted to competitive markets like Tier 1,2 cities and relatively slow growth.

What can go right?

Specialized, operations-centric business with a high throughput rate.

High margins are possible in key centers after reaching a critical mass (number of open loan accounts).

Established consumer behavior.

What can go wrong?

High upfront Capex is required for expansion.

Capital costs are higher for new entrants and smaller players.

High CAC (constant spending on branding/promotion as gold loans is a ‘need-based sale’ product) can hurt margins for smaller players.

Fintechs

This particular sector has seen lesser interest from fintech entrepreneurs compared to unsecured lending products. The size of the market opportunity notwithstanding, models like BNPL, credit cards, and personal loans have seen more startups and consequently more inflow of venture capital.

The existing players in this space can broadly be classified into two types:

Distribution first players: These are companies that are adding a layer of convenience to the gold loan process and digitizing the borrower journey for faster processing and trying to eliminate the need for captive physical branches. Prime examples in this space are Rupeek, IndiaGold, Ruptok, and YellowMetal.

Aggregator players: These are companies that are trying to enable partnerships between the various stakeholders in the value chain (valuation officer, storage, lending co. through technology to enable a network of credit across wider geo. Examples in this space are BharatPe (pilots), Bold Finance, Gold Setu. It's early days and there are no established businesses yet in this space.

Distribution First Players:

These companies are building technology-first platforms to digitize the gold borrowing process. The key aim here is to offer gold loans at the customers’ doorstep and acquire, process and close the lending cycle within the app itself, thereby minimizing the physical effort required for availing the gold loan.

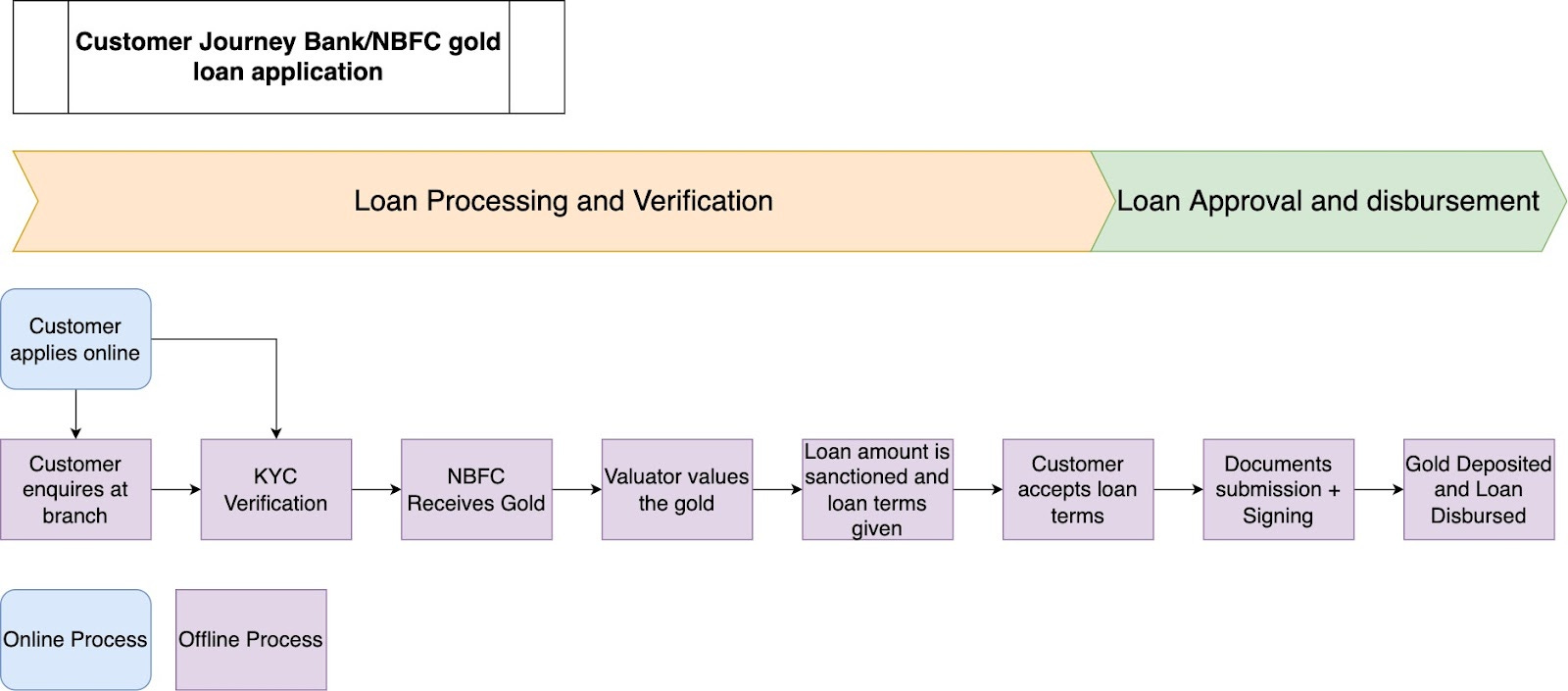

Here is the typical user flow in a digital gold lending co.

The companies in this sector source their capital from lending partners like banks and NBFCs and manage the entire customer cycle of valuation, storage, collection, and recovery for them.

They have invested in technology to convert the physical journey into a digital one. Key parts of this ecosystem are the robust app/web-based portal for customers to enquire, request, and close their loans as well as view their outstanding amounts and make payments, APIs to integrate with the lenders/NBFCs, eKYC protocols, and payment disbursal. They have also implemented field force management, route planning, and geofencing software to direct the valuation officers and ensure the safe handling of the gold.

Who wants Gold Loans in India?

You must be wondering after talking so much about who lends and how lending against gold happens, the most pertinent question remains. Who in India likes taking loans against gold. The answer is "a LOT OF PEOPLE". Let's dig in to see how does a typical customer of gold loan looks like.

The borrower profile can be classified into three broad categories:

Looking at customer segments who like gold loans and how they behave, you can make a few observations:

Due to the social stigma attached to gold loans, most borrowers tend to first exhaust all other lines of unsecured lending before tapping into their gold holdings.

Borrowers prefer to opt for gold loans only for short-term loans. More than 75% of the loans disbursed are in the 1 to 6-month tenure range.

The top factors for decision-making on gold loans are:

Interest rates and Loan to Value (LTV) ratio.

Flexible loan terms.

Ability to pay in lump sum or installments with no penalty.

Processing and misc. Fees.

Documentation - min. documentation and ‘no-source check’.

Due to increased migration in the last 20 years, a lot of borrowers do have ancestral gold holdings, but not at the point of borrowing. This limits the opportunity for fintech cos to tap into the opportunity.

Given these observations and ground reality, the ideal customer profiles for these are early/mid-level salaried employees, all categories of petty traders, and self-employed and SME business owners.

Gold Holdings

At any given point in time, the borrowers hold about 65% of their gold holdings for the express purpose of investment or usage in case of an emergency (35% as daily usage ornaments/jewelry). Gold lending companies typically maintain a 60-65% LTV ratio depending on the quality of the ornaments. Hence, average ticket sizes in this segment usually range from INR 2-4 lakhs.

Unit Economics

Most of the players in this category don’t lend. Instead, they act as loan originators (lead gen cos) and hence have to part with a lion's share of the interest revenue with the lending company. Their take rate may vary between 5-15% depending on the lender, area, borrower profile among other factors.

As per industry estimates, the cost of customer acquisition for fintech companies is around INR 3000 per organic customer (and increasing because they are all bidding on the same key AdWords).

The cost of organizing pickup and deposit of the pledged gold will be around INR 3,000 - 4,000 depending on the area and radius of operations for the valuer. Locker and Insurance costs will add a further INR 500 to the COGS.

The interest rates charged by the lending companies vary from 1.29% to 1.75% depending on factors like tenure, payment flexibility, and foreclosure and default penalties involved.

Considering the ticket sizes and interest rates, the digital lending companies can be expected to earn a revenue of INR 13,680 per deposit.

With a take rate of 5-15% (revenue sharing with the lending company); it is hard to see how digital lenders can break even on a unit economics level until they can achieve a certain level of trust/recall (similar to the star NBFCs) and acquire high ticket size, high repeat borrowers in high-density clusters.

Players like Rupeek have started lending from their books recently. Here, the cost of capital is a critical aspect, as it remains to be seen if they will be able to access abundant cheap capital to maintain competitiveness in the interest rates offered.

Another aspect is to understand the difference between rural and urban demand. With the rise of gig economy platforms and unsecured digital lending cos., the urban demand for gold loans may not grow in step with the rural demand. Hence, the companies can focus on growing in smaller Tier 2+ clusters where the demand is serviced primarily by local unorganized pawnbrokers and acquire customers by offering a superior service. However, due to the lower ticket sizes in the rural sector, it is advisable to have the strong operational expertise to ensure positive unit economics.

What can go right?

Physical to digital journey provides comfort and convenience to customers and does away with the social stigma attached to pledging gold holdings.

Multiple lending partnerships and ‘neo-bank UI’ are a net positive for the customer experience and can lead to competitive rates and increased repeat rates.

Integrating modern tools like IndiaStack (UPI, eKYC, Account Aggregation) can lead to building strong NTC (new to credit) customer profiles and hence increase the overall credit pool.

A large part of the value chain is handled by the Fintech Co. and hence there is no risk of over-dependence on a lending partner.

What can go wrong?

Creating trust with both lending partners and borrowers. Lack of access to trained personnel can lead to potential gold valuation fraud and lack of access to secure storage facilities can lead to loss of assets.

Ensuring positive unit economics with the current model seems like a challenge with prima facie evidence. This restricts the operational scope of the lending companies to high-density clusters and high ticket sizes.

This type of customer (high ticket size in Tier 1-2 cluster) also has access to other overlapping credit facilities and hence, there is a possibility that this can lead to increased customer acquisition costs and lower repeat rates.

Continued access to cheap capital is a necessary condition for the lending companies to maintain positive unit economics and remain competitive against specialized NBFCs.

Competition from Small finance banks and specialized NBFCs who have also started offering similar doorstep loan services (ref Muthoot Finance, SBFC).

Aggregator Players:

Aggregator Players are using a slightly different approach with the same goal of monetizing the idle gold holdings in Indian households.

Unlike distribution players that manage their field force of valuation and collection representatives and storage facilities; they are interested in operating as system integrators and aggregating the various stakeholders like collection points, storage facilities, and lending partners onto a single technology platform; providing the same ‘neo-bank UI’ and superior customer experience to the borrower.

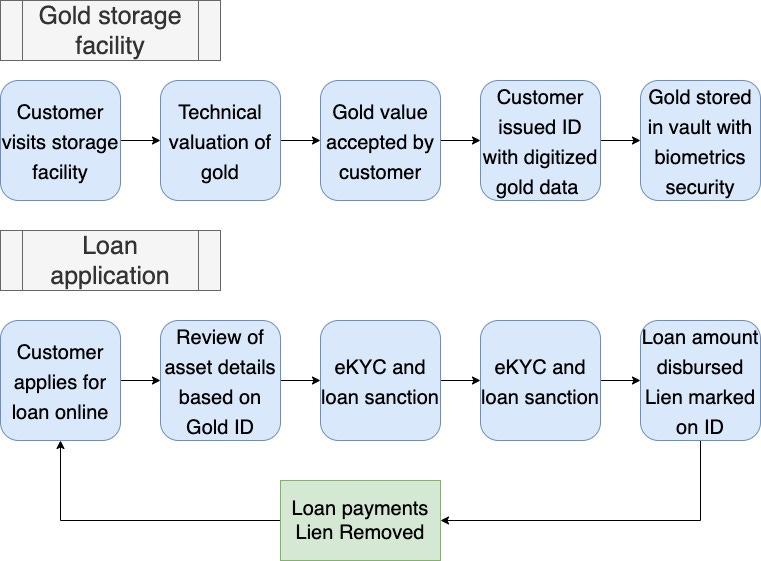

A good example in this model will be Bold Finance, a company I am personally tracking; which is building partnerships with local jewelry shops and onboarding them as physical branches for their lending business. Customers can log into the app and view all the partner stores in their location. Once they locate a store of their choice, they can walk into the store and get their gold loan processed in less than 2 hours.

The store is outfitted with a platform for customer onboarding, gold assessment, and eKYC. Once the loan is approved, the borrower gets the amount into a bank account of their choice. The store owner is responsible for the valuation process (it is not clear at this stage if this is a manual process with certain protocols in place or a machine-driven process with the help of gold assay meters) and the secure storage of the gold.

Lending partners are plugged in the backend, like in the case of distribution players who can disburse the capital based on the particulars of the borrower.

Customer Profile

These companies are also targeting the same demographic of customers as the distribution players with similarities observed in ticket sizes, loan tenures, and interest rates.

Unit Economics

As this kind of model is relatively new and the players have been active for less than 6 months, it is hard to understand the unit economics without venturing deep into assumption territory.

Broadly, since the cost of customer acquisition, the take rates, and the cost of storage and insurance remain the same; the major difference is observed in the (lack of) operational costs.

While the take rate will be split between the lending company and the franchise owner, this loss is offset by the reduction in operations costs.

Taking the same numbers as we did previously, the revenue per user can be estimated to be INR 13,680 with a take rate of 5 to 7.5%.

Considering the ‘asset-light’ model, it is safe to assume that the cost of operations will not increase with scale and hence, lead to positive unit economics in the long term.

Since growth/expansion is not determined by the availability of trained personnel or storage partners, this model enables the lending companies to grow faster and also to reach the credit-starved population in Tier 2+ towns in a profitable manner.

What can go right?

Physical to digital journey provides comfort and convenience to customers and does away with the social stigma attached to pledging gold holdings.

Tying up with local partners enables the companies to build trust easily.

Multiple lending partnerships and ‘neo-bank UI’ are a net positive for customer experience and can lead to competitive rates and increase repeat rates.

Companies that engage in pure technology play can capitalize on low ticket size, low-density clusters, and rural demand. This can lead to building strong NTC (new to credit) customer profiles and hence increase the overall credit pool. This can also lead to strong brand recall and upselling of other products in the future.

What can go wrong?

A high risk of fraud and false valuations is possible because of the franchise-owned and operated model.

High risk of broken/bad customer experiences because of the system aggregator approach. (Ref Oyo customer complaints)

The system aggregator approach leads to high dependence on various stakeholders like lending partners, credit franchisees and makes it tougher to move to a ‘full stack’ model.

Continued access to cheap capital is a necessary condition for the lending companies to remain competitive against specialized NBFCs.

What’s next

Competition from substitute products

Although the market size implies immense headroom for growth and few competitors in the digital gold lending space; I believe that the market, in general, is trending towards unsecured lending products.

The key reason behind this shift in the market is that the customers who had to earlier resort to pledging gold to fund emergency cash shortages are now able to avail of other financial products like BNPL products, credit cards, PoS loans, etc. Other Fintech lenders are encroaching on the borrower pool by leveraging platform behavior data and alternate credit scoring models to enhance their lending capability. BNPL loans, personal loans, and unsecured credit cards have especially gained in popularity in the last 3 years.

Maturing Alternate credit assessment models

A key development in the fintech space is the ability to develop advanced underwriting capabilities agnostic to the availability of credit history data of a customer.

This has become possible due to various regulatory interventions like the introduction of India Stack (Aadhaar/Pan integration), Account Aggregators, and ready access to platform data (Income data in case of freelancer/gig economy employees).

Although many fintech players faltered in the first phase with underwriting and had to write off loans; the underwriting algorithms have improved significantly over the last 3 years and the ratio of NPAs for unsecured lending fintech products is within the benchmark limits now.

This can lead to a massive increase in the borrower pool for unsecured lending fintech players in the future.

Need for portfolio diversification

In the last few years, the star lenders in this space have been exploring other opportunities to push for growth as they are experiencing saturation in the core business. This has pushed them to explore other verticals like housing loans, MSME loans, and other cash-flow-based lending products.

Gold-based lending fintech players should also take a leaf from this playbook as it will be key to establishing a strong brand name and ensuring high repeat rates from the existing customer pool leading to better unit economics.

Asset-backed lending platforms

Existing gold lending fintech companies can effectively utilize their technology capabilities to diversify into asset-based lending platforms that deal with different categories of assets. The companies can leverage the same infrastructure to branch out into other assets where a physical verification of an asset is a necessary condition before processing a loan application. Examples include new and used 2, 4 wheelers and commercial vehicles, property, and industrial machinery. Fintech companies can offer tagging and verification of physical assets as a service to other lenders.

Secured credit cards

An interesting approach to gun for better unit economics in the current business is to offer credit cards secured by the customers’ gold holdings. Continued usage of the credit card leads to better unit economics.

The convenience/benefits offered by credit cards might attract a new segment of customers who were previously ineligible/wary of credit card usage.

Rewards systems (partnerships/offers on aspirational purchases) can act as a strong differentiator and moat in the long run against competing players.

Gold Credit Networks

Gold asset-based open credit networks can help solve two problems: the need for safe and secure storage facilities for households and the facility to access credit based on the deposited assets. Customers can be incentivized to place the infrequently used gold ornaments and other holdings in a secure storage vault after a one-time assessment and then can access credit based on the data at any partner lending institutes (gold data as an API for lending partners).

This can create a strong database of both NTC and repeat borrowers, this will enable the companies to be able to sell them multiple targeted financial products based on their needs and financial profile in the future.

This is an infrastructure level play and will need significant investments in upfront Capex for investing in a network of storage facilities similar to the branch investments undertaken by specialized NBFCs in the early 2000s. The advantage of this model is that the investment in infrastructure creates a significant moat for the business (multiple strong regional level players) and it will not be easy for competitors to replicate success in the same clusters.

Gold lending is an interesting yet challenging and complicated business. Digital companies in this sector should observe the headwinds and optimize for higher customer retention, better unit economics, and a diversified asset portfolio to stand a chance at becoming a strong regional/national financial services player.

If you would like to discuss the lending market or exchange notes, we can connect over a call!

Depth of information and details are amazing.