#2 Will India Buy Now, Pay Later?

#2 Will India Buy Now, Pay Later?

The rise and rise of BNPL in India

INDEX

Overview

The Opportunity

Business Models

Rails Based

Open Loop System

Closed-Loop System

Distribution Based

Banks/NBFCs

Payment Processors

E-Commerce Marketplaces

Fintechs

Revenue Streams

Customer Side

Interest Income

Late Payment Charges

Transaction Fees

Merchant Side

MDR Fees

Merchant Commission

Unit Economics

Way Forward

In our previous essay, we established that one of the threats to gold loans was the emergence of unsecured lending products.

Most of us decry BNPL as a glorified credit alternative and wonder about its uses.

If you are following the trend of unbundling of banking services and ongoing consumer credit market liberalization, “buy now/pay later” (BNPL, for short) has become an inescapable trend.

This has become an umbrella term for a variety of products and services that offer consumers credit, both to enable/increase purchases and to encourage customer loyalty.

Overview

Merchants have been offering consumer credit in various forms in response to unusual credit environments (think Great Depression, 2008 Economic Crisis) has a long history in retail. Some of the more popular forms of credit have been the following:

Installment finance- Typically for consumer durable goods like electronics, appliances, and furniture. It is usually offered as a long-term (1-3 years) interest-bearing loan, potentially in combination with a promotional rate (eg, 0% for 12 months).

Store Credit Card- White label retailer-sponsored credit cards that have lower credit limits and typically looser credit policies. These enable and encourage larger customer purchases (Average Order Value, AOV) and drive customer loyalty; card programs also generate data for retailer marketing programs. Major retailers in India like Future group and Tata group run their own credit card programs.

PoS Lending- This model is based on using the retail customer as the lead for originating the loan. POS lenders typically tie-up with lenders to leverage their distribution. PoS lending is used for typically larger purchases with longer durations and requires a credit check. Bajaj Finserv is the undisputed leader in this space.

BNPL- This model also involves using the retail customer as the lead for originating the loan. Typically used in e-commerce transactions and smaller purchases. Involves minimal/soft credit check. There is no interest or fees to the user (if paid on time) and typically, the user pays 25% at the time of purchase and three additional payments in two-week intervals (Pay in 4 models).

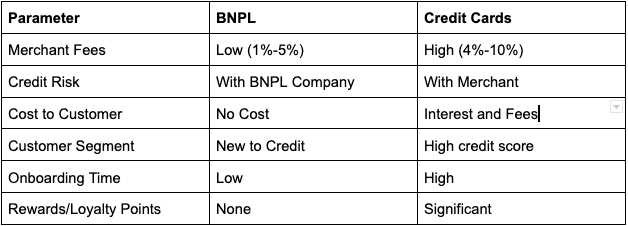

Key differences between BNPL products and Credit Cards.

The Opportunity

425 million active internet users.

150 million online shoppers.

35 million credit card users.

These 3 numbers put into perspective the size and scale of the e-commerce market and the opportunity that the BNPL players are going after.

As per HDFC Securities, India’s Buy-Now-Pay-Later (BNPL) is positioned as a source of gateway credit and poised to grow to USD56bn by FY26 (~5% of digital P2M payments) on the back of rising e-commerce and digital payments penetration.

Key factors influencing the growth in the BNPL sector:

Consumer-grade UI- Unlike in the case of credit cards and other personal loan products, the ease of signing up and availing of a BNPL line of credit is a major differentiator. In most cases, the user only has to set aside a couple of minutes during the checkout process to apply for BNPL credit whereas they will have to spend at least a couple of hours (if not more) applying for credit cards or personal loans.

Transparency- Users have a tendency to be wary of credit cards and the associated hidden charges because of the lack of transparency in product communication. In the case of BNPL credit, most terms are declared upfront in a clear and concise manner and they are easy to understand. This is especially important in the case of new to credit consumers and the target segment of Gen Z and young millennial users.

Better E-commerce experience- Merchants are eager to engage with BNPL partners as they lead to an overall positive shopping experience for the end-user. They can reduce cart abandonment by providing the option to pay for a product in multiple installments. User research also indicates that the average order value on a merchant site increases after the introduction of a BNPL partner.

Brand loyalty- As the merchant and BNPL partner can track the spending patterns of a cohort of users; this data is used to tailor-make credit offerings bundled with offers. This increases customer stickiness and brand loyalty leading to improved margins for the merchant.

The total funding raised by this sector is about USD 590m with Slice, Uni, Zest, and Simpl being the most funded players in the category. Large players like Bajaj Finserv, Amazon, Flipkart, and PayU also have their horses in the race.

Key Players

Business Models

There are a wide variety of products that come under the BNPL banner and they can be classified based on whether they are offered to consumers or businesses (B2C/B2B), based on how they are tapping into the merchant ecosystem, and also on their primary method of distribution.

Based on rails:

Since BNPL players use the merchant ecosystem for generating leads, the way they tap into the merchant ecosystem leads to two primary business models. The open-loop players tap into existing rails such as cards or UPI and even offline PoS whereas the closed-loop players work with deep integration with the merchants. The open-loop network, although easier to adopt and scale, provides little competitive moat as it is easy to replicate and difficult to ensure customer stickiness. The merchant fees they are able to charge are also lower in their case as they are competing with other players like credit cards and are forced to price at par with those players.

Based on distribution:

On a distribution basis, BNPL players can be classified based on the nature of distribution they utilize to acquire new customers. Each of these models is different in terms of the target customers, balance sheet exposure, etc. While incumbents, payment companies, and e-commerce marketplace players tap into their captive customer base, standalone FinTechs rely completely on open-market sourcing.

Revenue Streams

Revenue for a BNPL player can be sourced from both the customer side and the merchant side.

Customer Side:

Interest Income- Most BNPL players have a short interest-free period (1-3 months) and a subsequent loan tenure where they charge an APR of ~24% for a period of up to 12-18 months. This is common in the case of white goods, consumer electronics, and travel packages. For smaller ticket sizes like in the food, entertainment, and fashion categories the interest-free period is in the range of 15-30 days with a tenure of up to 3 months.

The interest rates on EMI loans offered by the BNPL players are higher than that of credit card and debit card EMI due to the higher risk profile of the customer, higher cost of capital, etc.

Late Payment Charges- Most BNPL players cannot offer a revolving credit option, hence, when there are delays in payments they tend to freeze the accounts until the dues are cleared. They also charge late payment fees and penalty charges based on the outstanding amount and period. Late fees as a percentage of spending are higher than that of credit cards.

Transaction Fees- Some BNPL players also charge a transaction/convenience fee for using the platform. Although, these fees have been tending towards zero in the last two years owing to the increased competition in the space. For instance, Mobikwik charges a one-time activation fee of Rs. 99 and Flipkart PayLater levies a convenience fee of Rs. 10/bill on bills above Rs. 1000.

Merchant Side:

MDR Fees- The merchant discount rate (the rate charged to a merchant for payment processing services on digital transactions) is low-hanging fruit in the spectrum of revenue streams. On the other hand, the MDR fees are usually benchmarked against the credit card processing fees and average out at 1.5-2% of the transaction value. This spread is usually used to provide discounts on various platforms to attract users for the BNPL product.

Merchant Commission- The key value proposition of BNPL players (other than the aforementioned credit offering) is increased sales velocity, higher average order value, frictionless checkout in e-commerce, and high customer stickiness. These traits are especially valuable to merchants who have relatively high gross margins and high costs of customer acquisition.

These merchants should be high-value targets for BNPL players as they can be high LTV customers and provide generous merchant fees. Merchant categories in the “high and medium willingness to pay” bracket are likely to provide higher merchant commissions to the BNPL players.

While assessing the health of a player in this category, it is worth noting that the revenue mix should be skewed in favor of the merchant fees rather than the customer fees. Excess contribution of late fees and interest charges in the revenue mix point toward a low-quality asset mix and delinquent behavior in the borrower pool.

Unit Economics

Most of the players in this category don’t lend. Instead, they act as loan originators (lead gen cos) and hence have to part with a lion's share of the interest revenue with the lending company. Their take rate may vary between 3-4% depending on the lender, area, and borrower profile among other factors.

The incremental cost of acquiring one customer is lower in the case of closed-loop BNPL players as they have partnerships with the merchant and more often than not, the exclusive credit partner at the Point of Sale.

The cost of customer acquisition for the open-loop players is higher as they need to compete with other BNPL players as well as credit card players to acquire a customer.

For the purposes of calculation, we can assume the average rate of interest for EMIs to be 24%, the MDR to be 1.5% and the merchant subvention for interest-free EMIs to be 3.5%. The cost of capital for most players is an average of 11% APR.

If we assume that delinquent behavior is minimal and a majority of the users pay back their borrowed amounts on time; the main revenue streams for the BNPL fintech are the MDR fees and merchant subvention fees. MDR fees remain in the 1.5-2% range as credit card MDR is often taken as the benchmark. Merchant commissions are usually restricted to higher margin and high tenure products. Benchmark peers in international markets like the US, Sweden, and Australia receive 4% to 6% in merchant commissions, a situation which is not possible in a low price market like India.

Customer acquisition costs and credit costs are the key cost drivers for a BNPL player. The customer acquisition costs are lower because the player is acquiring customers from the merchant ecosystem. However, the average order value and tenure are also much lower leading to lower potential revenue from the users.

The cost of capital is also high for most BNPL players as they do not have the scale and hence cannot borrow efficiently from the capital markets. For example, the recent offering of non-convertible debentures floated by Quadrillion Finance (NBFC related to Slice Cards) to raise lending capital offered an interest rate of 13.5%.1

The BNPL market is still in its early stages and most players have not yet achieved critical mass in terms of the number of users and average user spending. The limited scope for merchant and user revenue streams and the high cost of acquiring customers and capital can act as an impediment to profitability.

I believe that similar to credit cards, an optimal mix of credit and convenience fees is necessary for a clear path to profitability for the BNPL players. A wide net of merchant ecosystem partnerships and tailor-made offerings will drive down user acquisition costs and offer a strong revenue model in the form of the interest income (from the customer) and commission (from the merchant).

Way Forward

Regulatory Issues

A lot of questions have been raised about the questionable business practices and asset quality of the BNPL players. Problems range from falsified loan application records, and identity fraud to non-disclosure of terms and opening credit lines, and conducting hard checks with credit scoring companies without explicit user consent.

Hiding behind slick user interface designs and fancy branding, the BNPL products try to trick their users into doing things that they don’t intend to do. Gamifying the application and check out process, adding a ‘community’ aspect, and not offering clear terms and conditions are some of the tricks in the playbook that these players use to push their users into spending more on the platforms, avoid price comparisons and sharing more data about themselves than intended.

There are also instances of BNPL players not informing their customers about the multiple lines of credit for small amounts being opened under their name and being reported to the credit scoring authorities. These lines of credit play havoc on the user's credit score and it can take years to recover from this.

Taking cognizance of these nefarious practices and various complaints, the RBI has constituted a new Fintech department with the express purpose of looking into the workings of BNPL players and setting up regulations for this space.2

Some of the proposed recommendations in the works at the RBI include more upfront disclosures on hidden charges and interest rates, mandating FLDG (First Loss Default Guarantee) agreements between parties with an upper cap of 15-20% of shared exposure and bringing BNPL loans under the ambit of short-term credit which would make reporting of loans to credit bureaus a norm rather than an option.

The RBI Fintech committee is also exploring certification of digital lending apps, audit of alternate credit scoring algorithms, and stringent e-KYC and data privacy norms.

While most of the proposed regulations act as hygiene factors and protect consumers from fraud and misinformation; the regulatory ban on FLDG agreements between Banks/NBFCs and fintech players can play spoilsport in the growth ambitions of many BNPL players.

Players like Zest Money and Slice Pay have acquired an NBFC license, through the subsidiary route, along with simultaneously entering into partnerships with banks and NBFCs. I believe more players in the BNPL segment will opt to go for their own NBFC licenses or risk being absorbed by larger entities with a lending license.

The BNPL segment is the fastest growing and most vibrant corner of the fintech ecosystem. As the sector matures, we are seeing players experiment with various products and business models to find the perfect balance between high customer engagement and sustainability. The rapidly growing e-commerce market and the increasing propensity for merchants to offer BNPL offerings at their point of sale will lead to a booming market for BNPL players and new ideas will keep emerging.

It is still early days, and BNPL is here to stay.

If you would like to discuss the lending market or exchange notes, we can connect over a call!